How to Complete Part IV of Form 990-EZ

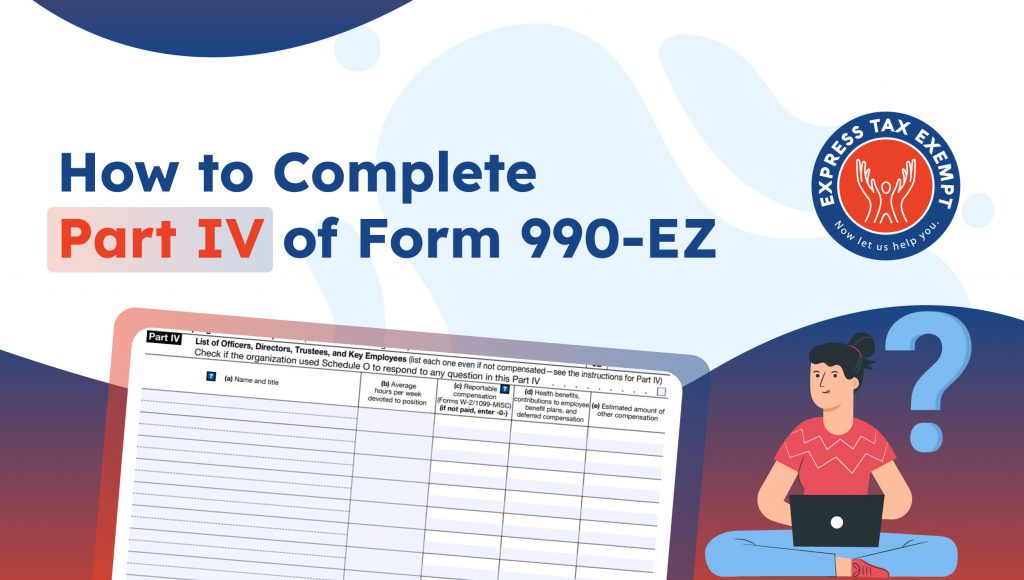

You’ve made it through part I-III of Form 990-EZ! Now it’s time to complete part IV. Part IV of Form 990-EZ is the List of Officers, Directors, Trustees, and Key Employees. This portion of the form is dedicated to the individuals that are involved in the governance of your nonprofit or tax-exempt organization.

When completing part IV of Form 990-EZ, you will need to list each person in the organization who was an officer, director, trustee, or key employee at any time during the organization’s tax year. You should list these individuals even if they didn’t receive any compensation from the organization. However, if they did receive compensation, you will need to report all forms of cash and non-cash compensation they receive during the tax year.

This will all be completed as you are filling in the necessary information for part IV. We’ve provided a helpful breakdown of Form 990-EZ part IV and the information you will need to provide:

First, let’s review some of the definitions:

The IRS defines an officer as “a person elected or appointed to manage the organization’s daily operations, such as a president, vice president, secretary, or treasurer.”

The IRS defines a director or trustee as “a member of the organization’s governing body, but only if the member has voting rights. The governing body is the group of persons authorized under state law to make governance decisions on behalf of the organization and its shareholders or members, if applicable.”

The IRS defines a key employee as “any person having responsibilities or powers similar to those of officers, directors, or trustees. The term includes the chief management and administrative officials of an organization (such as an executive director or chancellor).”

Time to Fill in the Information

Part IV of IRS Form 990-EZ has 5 sections of columns that you will need to fill. These columns consist of A, B, C, D, and E. Columns C-E deal with the compensation the organization’s officers, directors, trustees, and key employees received during the tax year. When completing columns C-E enter a zero (“0”) in the column if no reportable compensation or other compensation was paid during the tax year.

Column A

In column A, for each person that needs to be listed, enter their name at the top of each row and their title or position with the organization at the bottom of the row. You should list each person in the following order: individual trustees or directors, institutional trustees, officers, and key employees.

Column B

In column B, for each person you listed in column A, you will need to report an estimate of the average hours per week the person devoted to the organization during the year. You will need to enter a specific number.

Column C

In column C, you will need to enter the reportable compensation for the individuals you have listed. For officers and key employees, these amounts can be found in boxes 1 or 5 of Form W-2. For directors and individual trustees, the amount required can be found in box 1 of Form 1099-NEC and/or box 6 of Form 1099-MISC. Lastly, for institutional trustees, their reportable compensation is for services paid under a contractual agreement or statutory entitlement.

Column D

Column D requests that you report deferred compensation and benefits. Some examples of the deferred compensation and benefits you will need to report include, tax-deferred contributions by the employer to a qualified defined contribution retirement plan. Another example would be the value of health benefits provided by the employer that isn’t included in reportable compensation.

Column E

In column E, you will need to enter both taxable and nontaxable fringe benefits. However, you should not include compensation reported in column C or D. Also, you shouldn’t include working condition fringe benefits, expense reimbursements and allowances under an accountable plan, or de minimis fringe benefits. Instead, you should include the amount that the recipients must report as income on their separate income tax returns. You will also need to include payments made under indemnification arrangements, the value of the personal use of housing, automobiles, or other assets owned or leased by the organization.

After you’ve entered all of this information, you are finished with part IV!

E-file Form 990-EZ with ExpressTaxExempt

With ExpressTaxExempt, filing Form 990-EZ is quick and simple. Once you have created your free account and selected Form 990-EZ, simply…

- Add Your Organization’s Basic Details

- Add your Form 990-EZ information

- Review your Form

- Pay and transmit to the IRS.

With our helpful features and expert support team to assist you along the way, filing Form 990-EZ will be a breeze! If you need a refresher on completing part I, part II, or part III of Form 990-EZ, you can visit our previous blogs for helpful instructions.